The world economy is going through significant structural changes after many years of smooth globalization dynamics, which were altered by two huge global shocks: the pandemic and the Russia-Ukraine conflict. The timing and magnitude of monetary and fiscal policy responses to the pandemic differed across the globe and Russia-Ukraine has had uneven impact too. This has led to questions ranging from why growth is asynchronous to whether there are limits to fiscal policy. Here, we answer five of the questions we’ve been hearing from our clients about the changing global economy.

Around the world in 5 questions

Our new Head of Global Economics Research, Claudio Irigoyen answers 5 questions that have emerged as the global economy grapples with the aftermaths of these shocks.

Claudio Irigoyen, Head of Global Economics, BofA Global Research

Is global growth less synchronized?

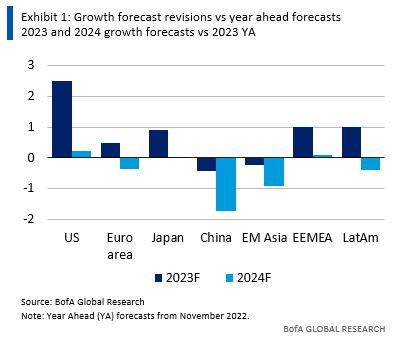

As the dust of the pandemic settles, we expect a mild global slowdown with less synchronized growth and inflation dynamics. We expect the U.S. to continue to lead growth and dictate the pace of interest rate moves globally. Japan is the big growth and inflation surprise, with implications for global rates. China is suffering a confidence shock and the government needs to come up with a comprehensive plan to stabilize expectations. Europe’s recovery will remain anemic. The global growth composition does not look favorable for EM (emerging markets), but Brazil, Mexico and India will likely keep outperforming, while ASEAN (Association of Southeast Asian Nations) is being impacted by China. Inflation risks are to the upside and central banks will keep rates high for longer, while China will continue fighting deflation.

Why is the U.S. economy so resilient?

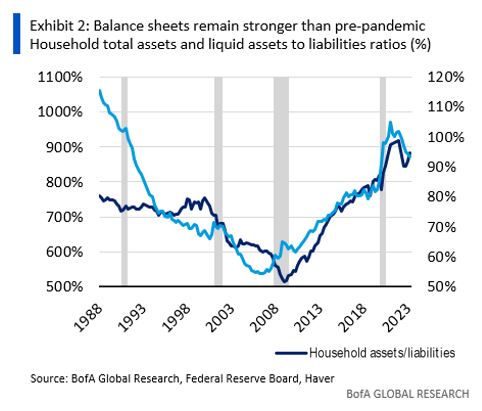

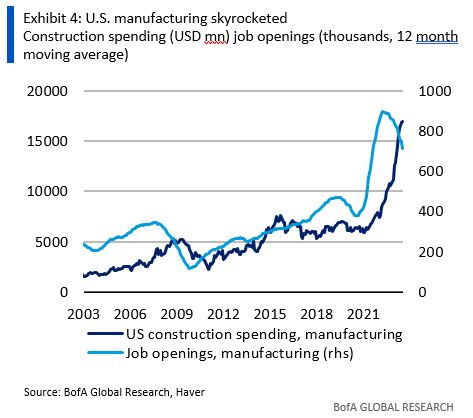

The resilience of the U.S. economy can be explained by essentially two factors: a faster-than-expected recovery in business investment and strong private consumption, fueled by a solid household balance and a tight labor market. Fiscal impulse was higher than expected. Households and corporates refinanced mortgages and debt when rates were low. Real estate prices are high due to lock-in effects. Risks are mostly related to higher for longer policies and excessively loose fiscal policy putting pressuring on interest rates.

What is different about Europe?

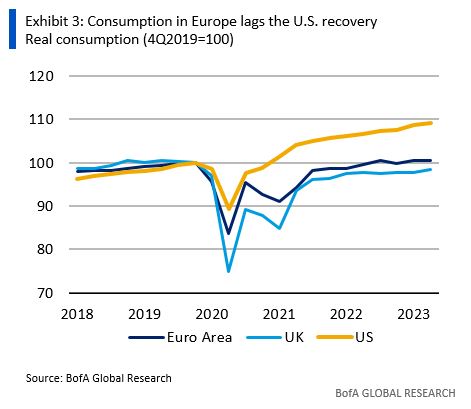

Europe is underperforming the U.S. and inflation remains persistent. The underperformance is both structural and cyclical. The energy shock hit Europe harder than the U.S. The size and composition of the fiscal response to the shocks explains the consumption boom in the U.S. relative to Europe, while the strength of investment in the U.S. is absent in Europe. Europe is more exposed to China’s slowdown than the U.S. Consumer sentiment is weak and excess savings remain high driven by precautionary motives.

Can we see geopolitics in the data?

Geopolitical alliances are changing the way countries trade and capital flows. China exports are shifting away from the West. Mexico is gaining share in U.S. imports. Reshoring and nearshoring are manifesting in the manufacturing boom in the U.S. and Mexico. U.S. FDI (foreign direct investment) is shifting out of China into ASEAN and LatAm. Next year, we have elections in countries that represent 63% of world GDP (gross domestic product), including the U.S., Mexico, India, and Taiwan. With polarization on the rise, we expect an increase in policy uncertainty.

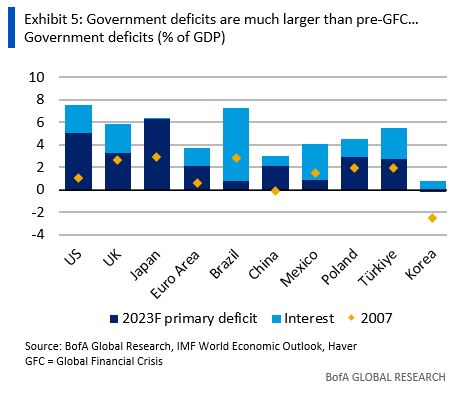

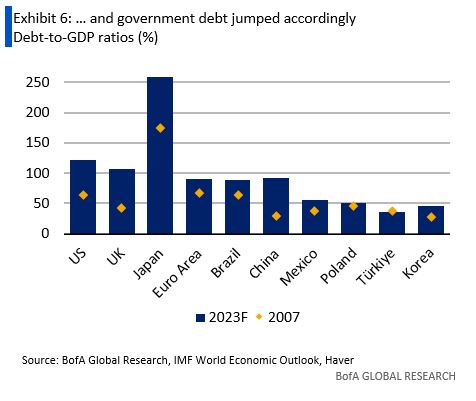

What are the limits of fiscal policy?

Fiscal policy deteriorated across countries post-pandemic and the increase in interest rates is threatening debt sustainability absent sizable fiscal consolidation. Fiscal policy is losing power to fight the next recession. Fiscal policy might end up conditioning the conduct of monetary policy. Fiscal dominance1 is not around the corner but is not light years away either.